Today, ACER publishes its Decision amending the European Resource Adequacy Assessment methodology, following the proposal submitted by the European Network of Transmission System Operators for Electricity (ENTSO-E) in November 2025.

What is the methodology about?

The ERAA, mandated by the Clean Energy Package (2019), is ENTSO-E’s annual assessment of the EU’s electricity supply adequacy for the next decade. Its purpose is to evaluate whether the EU has sufficient electricity resources to meet future demand and to identify potential risks to security of supply. Each year, the assessment is subject to ACER approval.

At national level, Member States define their own reliability standards (based on ACER’s methodology) to set the level of security of electricity supply they require. The ERAA annual assessment provides a consistent, objective tool to evaluate adequacy risks against those standards and whether the introduction of national measures (such as capacity mechanisms) is needed.

Why amend the methodology?

In its streamlining report (March 2025), the European Commission requested ACER to amend the ERAA methodology to streamline the capacity mechanisms’ approval process. ACER subsequently required ENTSO-E to propose the necessary amendments.

In August 2025, the Commission also adopted the Clean Industrial State Aid Framework, which introduces a fast-track process for approving capacity mechanisms. To support this framework, the ERAA methodology needs to define the procedure for calculating, within the ERAA annual process, the parameters necessary for Member States to make use of the fast-track approval process.

What are the main amendments?

The updated ERAA methodology focuses on:

1. Supporting capacity mechanisms approval

- Introducing capacity mechanism-related parameters derived from the ERAA model, which Member States may use to benefit from the fast-track process.

These parameters:

- improve the clarity of ERAA results by quantifying the size of the adequacy concern (adequacy gap and total firm capacity needs) and how different technologies contribute to system adequacy (de-rating-factors);

- can be used by Member States to size their capacity mechanisms (when applying for fast-track approval).

2. Simplifying the methodology

- Focusing the model on key target years (instead of explicitly modelling every year of the next decade).

- Introducing simplified approaches for key methodological components (e.g. estimating flexibility resource revenues and developing scenarios that reflect the impact of capacity mechanisms across Europe).

- Streamlining how Member States’ efforts to avoid regulatory distortions or market failures are represented in the ERAA.

3. Improving adequacy modelling

- Developing a new Trends and Projections scenario to better reflect the actual pace of the energy transition.

- Improving the modelling of investors’ risk aversions and introducing a more realistic representation of flexible resources’ (e.g. batteries and demand response) business case.

What are the next steps?

ENTSO-E will progressively integrate the amended ERAA methodology into future ERAA reports (starting with the upcoming 2026 edition). As part of this implementation, capacity-mechanism-related parameters will be introduced in the ERAA framework. These parameters will help improve coordination of capacity mechanisms across Europe, increase their efficiency and help reduce costs for consumers.

Based on the ERAA results, Member States may also use these parameters when applying for the fast-track approval process for capacity mechanisms.

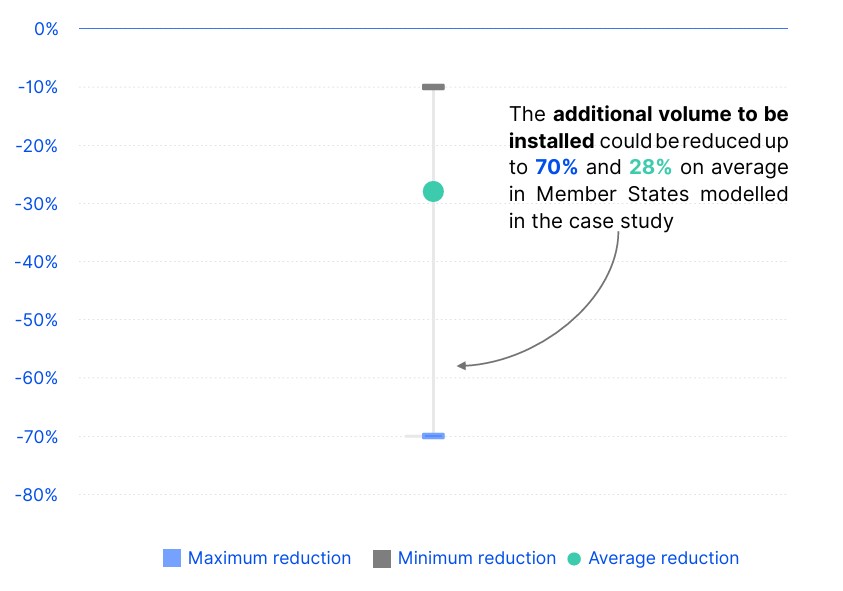

The image shows how coordinating capacity mechanisms across EU borders reduces procurement needs and lowers costs for consumers. Source: ACER Monitoring Report on security of EU electricity supply (2025).